Why do mortgages matter?

At a high level, mortgages are one of the key levers in the real estate market and integral to the homeownership dream for Americans. Whenever the majority of Americans look to buy a home, they go through the mortgage application process and continue to interact with their mortgage servicer until they payoff their loan. It’s also the largest piece of debt and obligation that the majority of consumers take out in their lifetime. So at a minimum, you can say that one of the biggest decisions a consumer makes in his or her life is taking out a mortgage and thus, is core to the American Dream.

On a more macroeconomic level, if you view mortgages as somewhat synonymous with the real estate market, then it’s one of the largest drivers of the US economy. Construction and remodeling of homes (which is funded by mortgages) is ~5% of GDP and consumer spending on housing services is another ~12-13%. Unsurprisingly, this results in the US government having a massive vested interest in stabilizing and propping up the housing market (think of what happened in 2008!). It’s also hugely instrumental in promoting social stability through the creation of sustainable communities that many spend their entire lives in (Urban Institute). We can go on and on but a more efficient, cost-effective, and transparent mortgage experience is beneficial to society.

Ecosystem

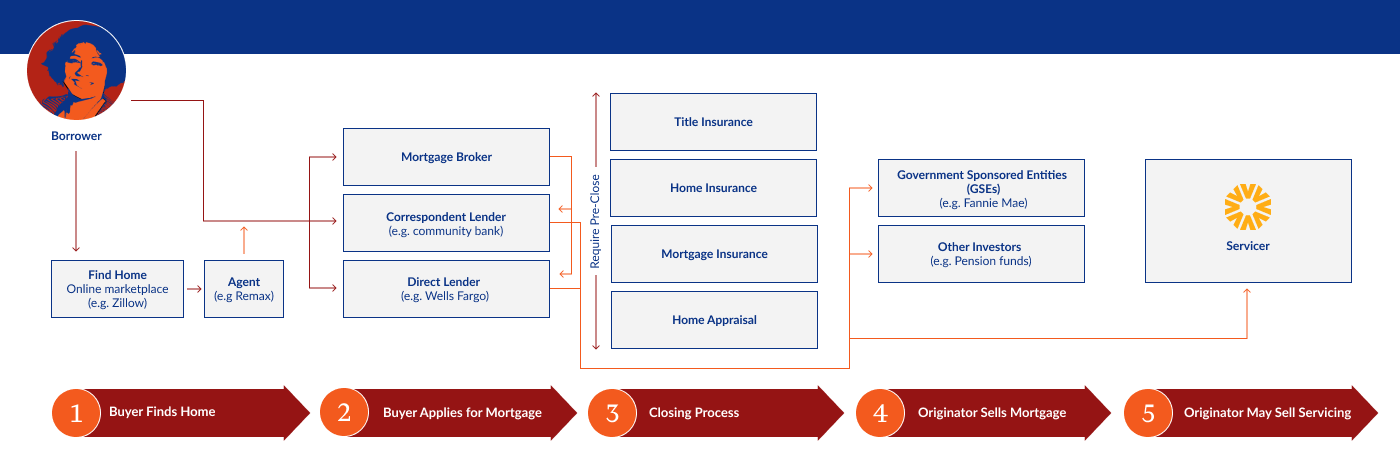

a16z’s Guide does a fairly good job of going through how the ecosystem works today so I’ll skip through the process of getting a mortgage. Feel free to read through to get a quick overview. What should be readily apparent is that there are a number of heavily entrenched players and processes that are involved and it takes some real industry experience to unbundle the entire mess.

For our business, the key players that we care about day 1 are:

- Mortgage Investors (GSEs or Other Investors above): these are the guys who ultimately end up owning the mortgage long term. This matters because they ultimately decide who does the mortgage servicing (hopefully us!).

- Mortgage Servicers: These are the guys who actually collect the P&I, insurance, and taxes from the homeowners and send it to the lender. They also handle the situation in which the homeowner is delinquent and needs to be modified, foreclosed upon, etc. Key players include Mr. Cooper (Nationstar), Wells Fargo, JPM Chase, Ocwen, Shellpoint, etc

- There is a further distinction between Master Servicers and Subservicers: Master Servicers are the entities who ultimately are engaging directly with the investor and are responsible for figuring out how to service the loan. Now, this is interesting because they can choose to not do the task themselves and contract it to a subservicer. In this situation, the subservicer is actually doing the work. The master can have multiple subservicers to handle different or similar portfolios to de-risk their reliance on any one subservicer. This arrangement happens because there are often requirements for the Master Servicer to be creditworthy, have a minimum net worth, or purchase the right to service a pool of loans, so some subservicers don’t want to put their capital to this use. On the other end, the Mortgage Investors only want to deal with one party so the Master Servicer is responsible for interfacing between their various subservicers and the Mortgage Investors to mitigate their concerns.

- Technology Providers: Servicers rarely build their own in-house technology and instead rely on outside vendors. These include Black Knight (their product is MSP), FiServ (Loanserv), CoreLogic, and Finastra. There are a variety of issues associated with these providers including (but definitely not limited to) slow support, non-modular structures, poor feature coverage, and lack of full integration.

- GSE (Fannie/Freddie/Ginnie): Government Sponsored Entities are the backbone of the mortgage market. They purchase a majority of qualified mortgages from banks and other lenders which they then insure and bundle into mortgage backed securities. In order to operate in this market, we need their approval for us to service their loans.

- CFPB (Consumer Finance Protection Bureau): Elizabeth Warren’s baby, this is the federal agency that creates rules around how mortgages are originated and serviced to protect consumers. You still have to deal with state laws and regulations but the CFPB governs most of the federal level issues. Doesn’t only deal with mortgages FYI.

- FHFA (Federal Housing Finance Agency): Regulator that sits on top of the GSEs and deals with all housing issues.

Types of Mortgages (QM / Non-QM / Conventional)

Conventional/Conforming mortgages are a category of loans with pretty standardized features. This makes it easy for investors to analyze and understand. In turn, consumers get a better rate and terms. You can read more about it here but you can largely think about them as highly regulated mortgages that Fannie/Freddie can buy and hence is cheaper. You cannot service these without a Fannie/Freddie ticket. This does not mean that non-conforming mortgages are much riskier – they’re just not as standard and therefore harder to relatively evaluate. For example, jumbo (larger size) mortgages can be non-conforming if they’ve exceeded the conforming loan limits. Similarly, FHA/VA loans can often be non-conforming. This is often used interchangeably with the term “qualified mortgage” or QM. Qualified mortgages are ones where the lender has done an ATR or Ability-to-Repay analysis. By doing this work, the government gives what’s called “safe-harbor” to the lender, thereby absolving them of liabilities if the homeowner defaults. Technically, any loan that has a DTI (debt-to-income) less than 43% is a QM or if it is GSE-eligible (Fannie/Freddie/FHA/VA). On the other hand, Non-Qualified Mortgages do not have these standardized features or homeowner profiles and hence, are outside of the bounds (and requirements) of the GSEs. Back pre-’08, these were the crazy loans that blew the US housing market up. Today, these are generally given to individuals who don’t fit the tight box that is QM (i.e. you are a non-salaried worker / contractor) and have low loss rates because investors have become very cautious. They also are easier to work with in the sense that the only qualifications that are necessary are state licenses and you only have to follow state and federal regulations.

The Problem We’re Trying to Solve

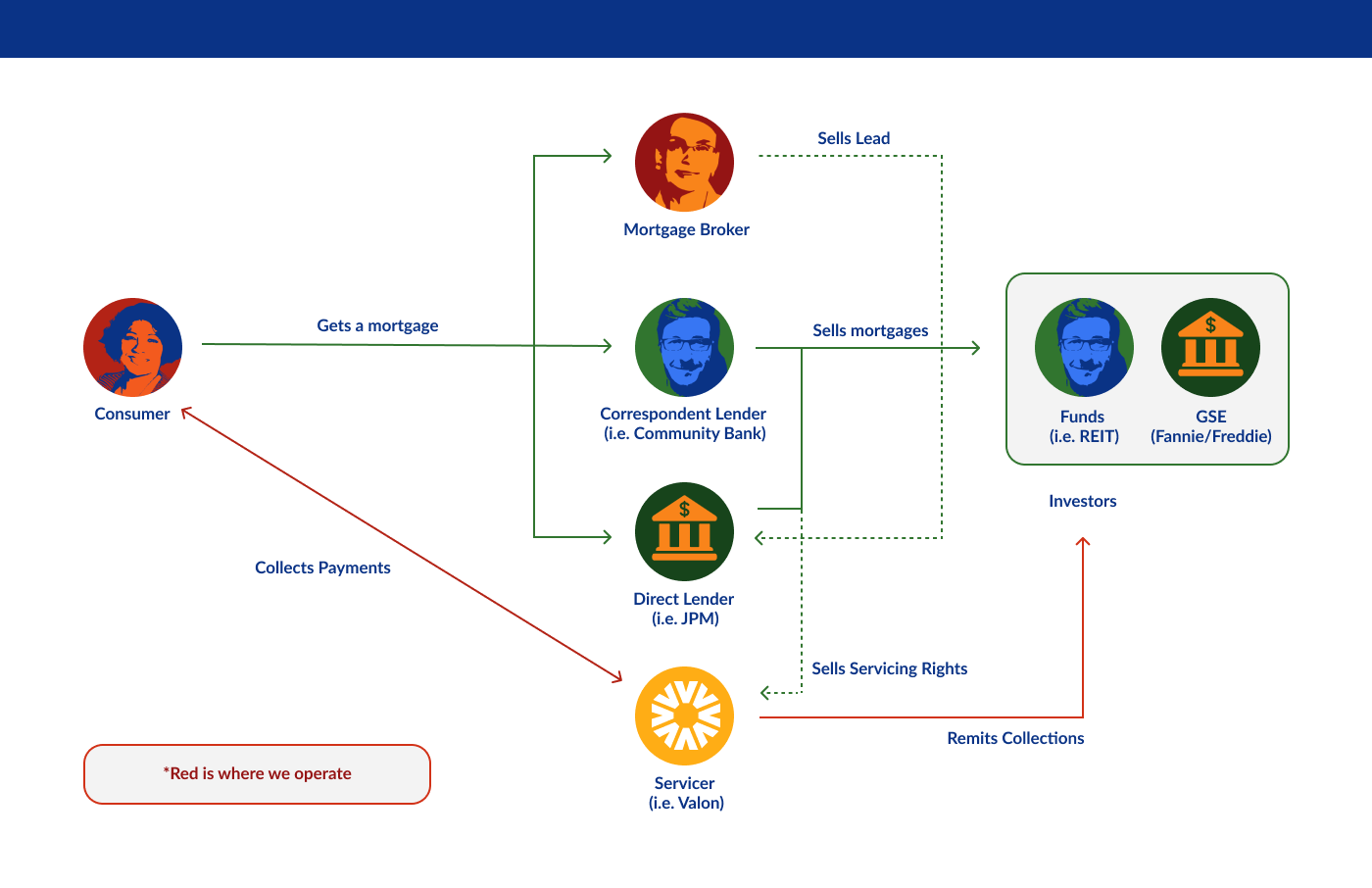

While many companies focus on the mortgage origination side of the business, we want to focus on the servicing side of the equation which happens to also be the long term customer relationship management component. Like we explained earlier, this is the part of business where the primary roles are two fold: 1) collecting payments (P&I, taxes, insurance, HoA) and 2) handling delinquencies and foreclosures. While there are a ton of problems with mortgage servicers, the net result is that they have gone from being 20-30% net income margin business to 0% margin business.

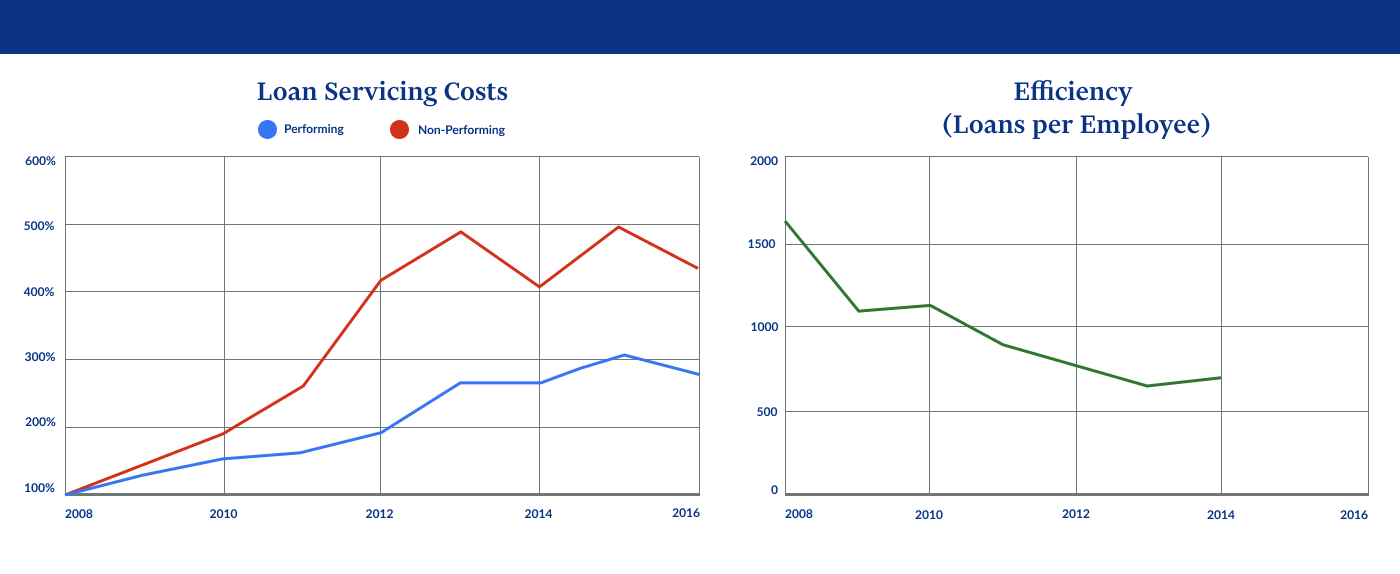

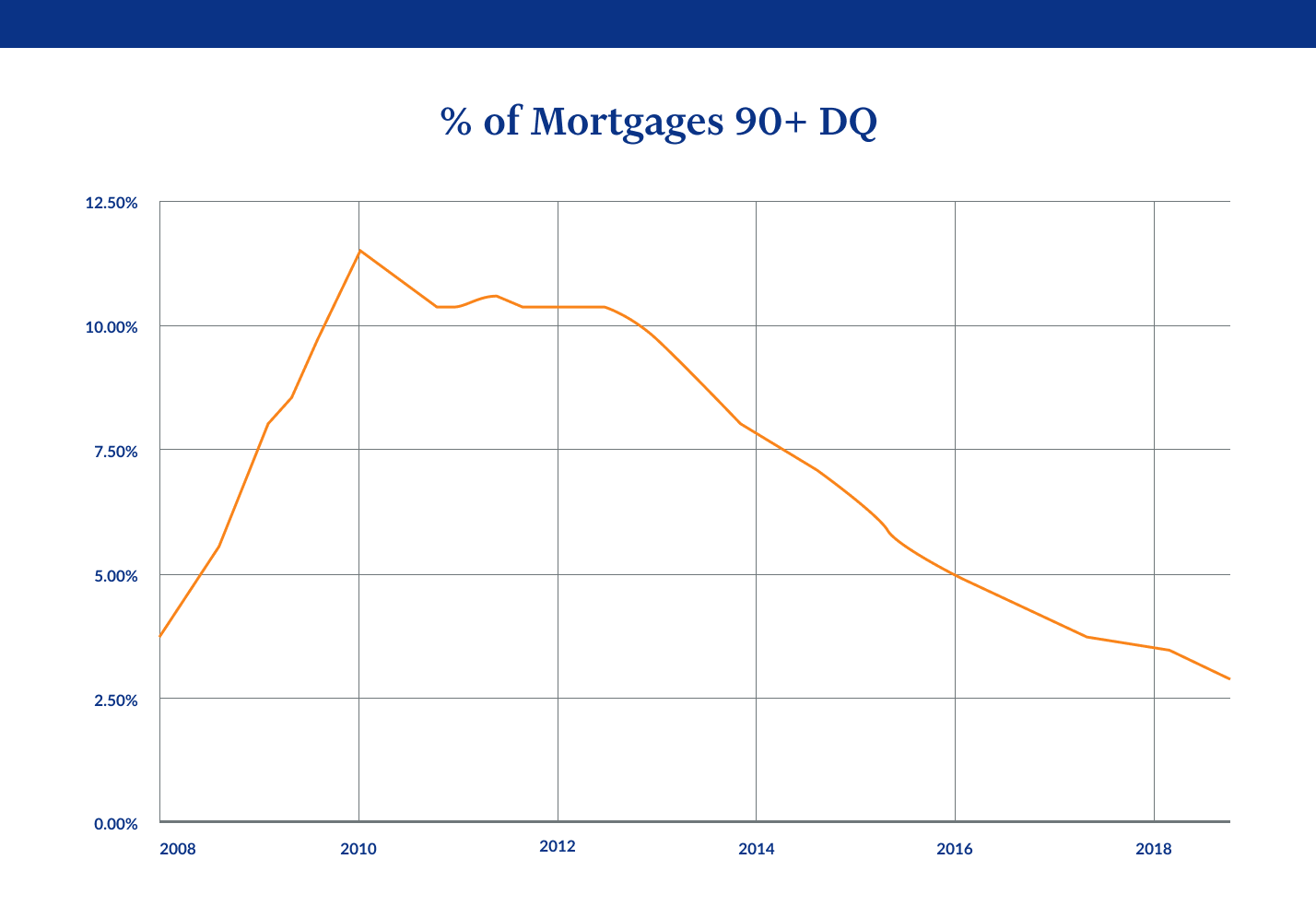

Why did this happen? When people look at the left chart only, they sometimes attribute the lower net margin of mortgage servicing strictly to the increasing cost of servicing delinquent loans—especially given that after the Great Financial Crisis there were a lot of delinquent loans.

However, this chart suggests that while there was a large increase in delinquency after the financial crisis, it has since come back down. Further, the initial Loan Servicing Costs chart itself clearly tells a different story—performing loans had a similarly large increase in costs. If you look at the proportional decrease in efficiency in the left chart, it matches the inverse of loan servicing cost increase of performing loans. This strongly suggests that there is more to the story than just simply mortgage delinquencies increasing.

Root Cause

Our belief is that the fundamental problem behind the decline of the servicing industry is due to poor data schema and service abstraction. It’s a problem we think is easy to sympathize with. Imagine if you were to build a mortgage servicing software from scratch without knowing much about the future regulation (or really much about the mortgage market). You would hard code all of the existing mortgage rules and regulations and once a loan has been instantiated, it wouldn’t need to be altered. This wasn’t a problem pre-crisis when the market did well and most loans that went delinquent were just foreclosed on(and perhaps even sold for a profit). However, post-crisis, a whole suite of new regulations started to come into play. Some were pending and some were ambiguous but failing to comply would definitely result in large penalties. So, ad-hoc solutions were layered on top of this existing servicing software, like hard coding new rules into the system. That worked well for loans going forward but what about old loans? Should the history change? Were there homeowners considered delinquent in the past based on the new rules? If you keep just the history and change the code, how do you go back and know why the loan was considered delinquent? Clearly, the old data models couldn’t handle this!

Here are some more example situations that causes problems for existing servicing software:

- SCRA (Servicemember Civil Relief Act)—when an individual becomes a service member, they are granted relief by having their interest rate capped to a maximum of 6%. A loan with a higher interest rate has to have its interest retroactively lowered to 6% based on the date they became a service member. In this example, a borrower’s future payments and whether or not they were delinquent in the past would change.

- Inconsistent regulation — New federal laws and state laws don’t always match with each other. Often there is federal preemption (i.e. federal applies over state) but you still can get in trouble otherwise. You can try to be safe and take the approach that is friendlier to the consumer, but what if they contradict each other? How do you track what regulation you decided to enforce and why?

- Disclosure tracking—there are disclosures that need to happen. What happens when the disclosure requirements change—how do you know what you actually complied with if you built in hard coded disclosures to begin with?

Now, there are other technology problems like missing features to complete servicing tasks, a lack of full integration between the numerous servicing systems required, and a severe lack of consumer transparency. All of these are independent pieces of the puzzle, but, as we pointed out in this section, the root of all of these issues is bad/outdated technology.

Some Symptoms

What’s the most straightforward result of bad technology? More people/overhead and hence, massive scale in order to get somewhere close to profitability.

Also, it generally means there’s a terrible consumer experience. Like no mobile and some clunky website.

Market Size

For a space that hasn’t seen innovation in so long, you would expect that the market just isn’t large enough to justify the resources and investment required. Fortunately for us, this is definitely not the case.

The rough math works like the following. There is $10.3T in UPB (unpaid principal balance) for residential mortgages in the United States. The minimum fee is 25bps annualized, which means we’re really talking about $25+ billion paid in fees to mortgage servicers yearly. This is a market that grows as real estate values grow and more housing is needed.

We’re not even adding on core servicing businesses of recapture and refinancing. For just refinancing, there is $500 billion transacted a year that you can earn an additional 1-3% of.

You can imagine how limitless the opportunity starts to look when we start layering on other value add services.

Conclusion

To recap, this is a massive space with real problems and non-trivial solutions. The history of the space and legacy infrastructure have trapped the incumbents in a quagmire that is not easily solvable. That said, we think it’s way past time for consumers to be provided with a transparent, friendly, servicing solution. It’s long overdue for regulators and investors alike to be provided with clear and powerful analytics to understand what is going on in their portfolios and the economy. And it’s time for there to be a software platform that leads product innovation and benefits the ecosystem as a whole. It’s time for Valon, the mortgage servicer of tomorrow.